Key Takeaways

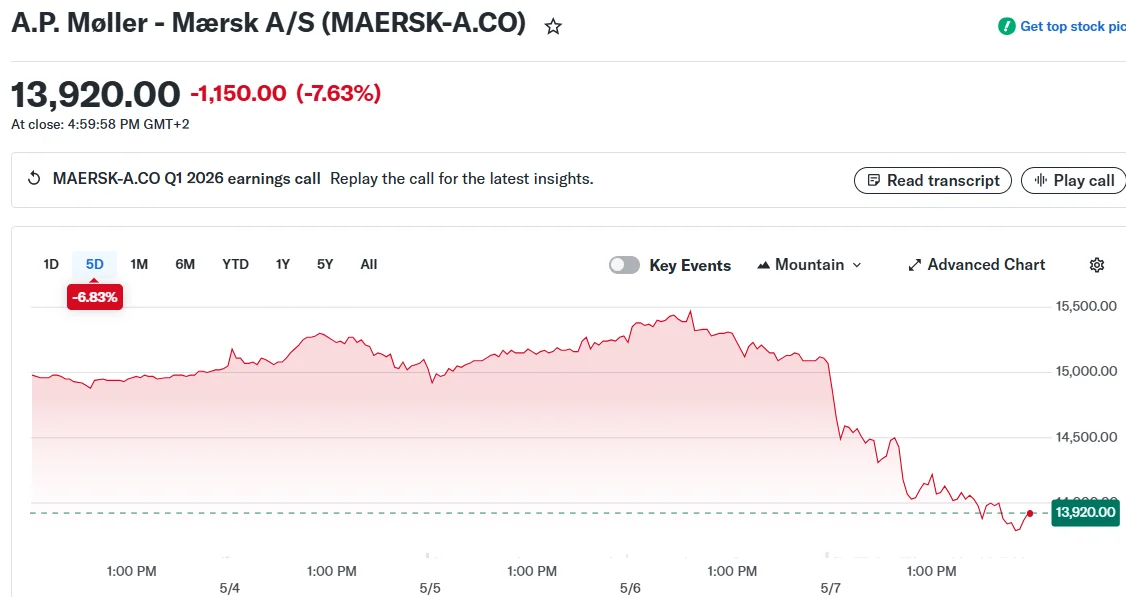

- Shares of Maersk declined 7.5% in Copenhagen following first-quarter financial results

- First-quarter EBITDA reached $1.73bn, surpassing analyst expectations of $1.66bn while trailing the prior year’s $2.71bn

- Annual outlook remains at 2%–4% container volume growth worldwide

- Strait of Hormuz blockade by Iran drives up energy expenses and operational complications

- Asia-Europe shipping rates have declined back toward pre-conflict levels despite elevated fuel prices

The Danish container shipping leader delivered quarterly results Thursday that exceeded analyst projections, yet investors reacted by selling off shares amid concerns about deteriorating market conditions ahead.

The maritime transport company posted first-quarter EBITDA of $1.73bn, topping the Wall Street consensus estimate of $1.66bn. This figure represented a significant year-over-year decline from $2.71bn recorded in the comparable 2024 period.

Shares tumbled 7.5% during Copenhagen exchange hours, while the broader market index remained essentially unchanged.

Shipping rates experienced downward pressure throughout most of the three-month period as vessel capacity continued to exceed demand. Rates only surged toward the quarter’s conclusion following the intensification of Middle East hostilities in late February.

Military operations commenced February 28 when coordinated American and Israeli forces struck Iranian targets. The timing means first-quarter financial data captures only minimal effects from the regional conflict on worldwide logistics networks.

Tehran’s closure of the Strait of Hormuz to merchant vessels has compelled carriers to seek alternative routes, inflating energy expenditures and upending traditional maritime corridors industrywide.

Middle East Crisis Maintains Cost Pressures

Maersk has redirected vessels around the African continent, bypassing both the Suez Canal and Bab el-Mandeb passage. This strategy represents a shift from previous intentions to progressively restore certain Suez route operations.

Chief Executive Vincent Clerc delivered a frank assessment of the energy landscape. “The energy crisis does not go away the day peace comes,” he informed journalists, noting petroleum industry projections for sustained elevated costs spanning “at minimum several more months.”

The shipping company maintained its annual projections, reaffirming expectations for worldwide container volume expansion between 2% and 4%. However, management emphasized that market conditions continue to exhibit instability.

Executives highlighted that rising energy prices combined with trading limitations in the Upper Gulf region — representing approximately 6% of worldwide container commerce in 2025 — create potential headwinds for achieving growth targets.

Financial Experts Express Caution on Outlook

Morgan Stanley research teams indicated they perceive “limited scope for earnings upgrades” stemming from the quarterly disclosure, suggesting any forecast adjustments will correlate with freight pricing trends.

Analysts observed that pricing on principal European shipping lanes has essentially eliminated gains accumulated since Middle East tensions began. Vessel deliveries continue exceeding demand growth — Maersk itself commissioned eight new ships during February.

Jyske Bank analyst Haider Anjum cautioned about potential downward guidance revisions later this year. “Freight rate developments are not expected to be able to compensate for the higher fuel costs,” his analysis stated.

Morgan Stanley identified one possible positive development: bunker fuel supply constraints, which might accelerate vessel idling decisions. Analysts acknowledged this scenario lacks current data support while emphasizing the importance of continued monitoring.

Management indicated efforts to transfer elevated costs to customers, though success remains uncertain given prevailing rate dynamics.

Asia-Europe corridor pricing has retreated nearly to pre-conflict benchmarks while energy costs remain inflated — a scenario analysts believe could compress profit margins in upcoming quarters.