Key Highlights

- Major U.S. equity benchmarks declined last week, Nasdaq shows 10% year-to-date loss

- Strait of Hormuz closure drives oil prices higher by more than 45% over 30 days

- March employment figures forecast to reveal 50,000–56,000 new jobs on Friday

- Consumer confidence drops to December lows amid geopolitical economic concerns

- Market participants now assign 22% probability to Fed rate increase by late 2026

Financial markets enter a condensed trading week facing declining equities, elevated crude prices, and employment data that may shape near-term direction.

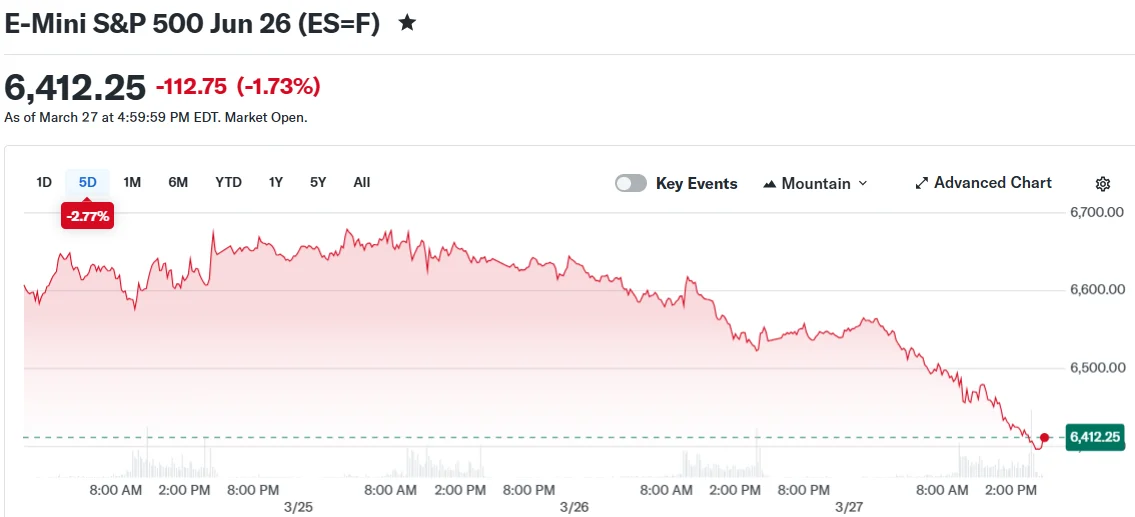

The S&P 500 retreated 2.12% during the previous week, settling at 6,368.85. The Dow Jones Industrial Average declined 1.73%, losing approximately 800 points during Friday’s session alone. The Nasdaq Composite dropped 2.2% on Friday, bringing its year-to-date decline to roughly 10%. Each of the three major benchmarks has moved below their 52-week moving averages, signaling a breach of technical trend support.

The primary catalyst remains the continued U.S.-Israeli tensions with Iran, entering their fifth week. The Strait of Hormuz stays effectively blocked, removing 15 to 16 million barrels daily from worldwide supply channels. Brent crude has climbed more than 45% while WTI crude has risen over 50% during the past month.

BP chief economist Gareth Ramsay characterized the Strait of Hormuz closure as “every analyst’s study piece, or worst nightmare that we thought could never happen.” Iranian parliamentary speaker Mohammad Baqer Qalibaf stated the strait “cannot be the same as before.”

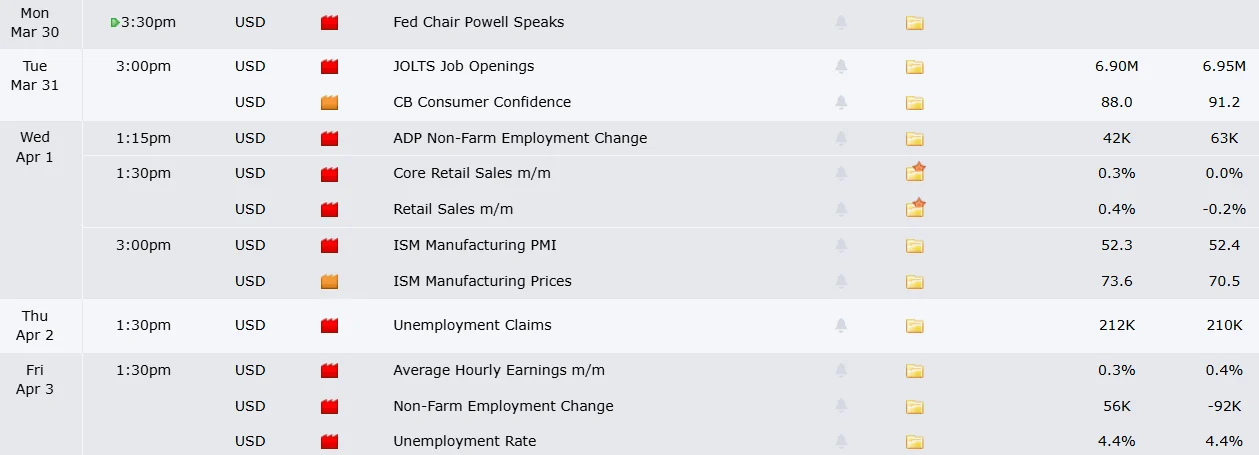

Employment Report Takes Priority

Friday’s nonfarm payrolls release stands as the week’s most significant economic event. Analysts anticipate approximately 50,000 to 56,000 positions added during March, following February’s sharp decline of 92,000 jobs. The unemployment rate is projected to remain unchanged at 4.4%.

Goldman Sachs economist Pierfrancesco Mei projects elevated crude costs will reduce monthly payroll expansion by roughly 10,000 jobs through December. BNP Paribas economist Andrew Husby noted a more substantial energy disruption would be required to shift the current pattern of minimal hiring and limited layoffs.

Ahead of Friday’s report, market participants will monitor consumer confidence readings on Tuesday, JOLTS job openings data, ADP employment statistics on Wednesday, and weekly jobless claims on Thursday.

Central Bank Policy Expectations Shift

Fixed income markets have begun incorporating expectations of a more restrictive Federal Reserve stance. The 10-year Treasury yield reached 4.48%, marking its peak since July. Two-year yields climbed to 4%, advancing more than 30 basis points following the Fed’s most recent meeting.

BofA Global Research economist Aditya Bhave observed that markets seem to be “anticipating a more hawkish Fed reaction function.” Market pricing now reflects a 22% probability of a quarter-point rate increase by the conclusion of 2026.

Headline CPI is projected to approach 3.5% on a year-over-year basis in upcoming months as pump prices near $4 per gallon across the nation.

Regarding corporate earnings, Nike delivers results Tuesday, with attention focused on Chinese market demand trends. ConAgra, Lamb Weston, and Cal-Maine Foods announce results Wednesday. Tesla plans to publish monthly delivery figures during the week.

Federal Reserve Chair Jerome Powell addresses markets on Monday, with participants scrutinizing his remarks for policy direction clues.