Key Highlights

- Friday brings the April employment data, with forecasts calling for approximately 60,000 new positions

- Chip sector reports from AMD and Arm Holdings offer crucial insights into AI investment momentum

- Major consumer brands like Disney, McDonald’s, and Marriott release quarterly results

- Record closing levels reached by both the S&P 500 and Nasdaq on Friday

- Technology giants’ AI capital expenditures have expanded to approximately $725 billion

Investors face a data-intensive week as April’s employment report arrives alongside a significant batch of corporate earnings, providing critical updates on economic momentum.

Both the S&P 500 and Nasdaq Composite achieved record closing levels on Friday. Weekly gains showed the S&P 500 advancing just under 1%, with the Nasdaq climbing 1.1%. The Dow Jones posted a 0.3% decline Friday but managed a 0.5% weekly increase.

Big Tech earnings dominated the previous week’s trading action. Five members of the Magnificent 7 released results, drawing favorable investor reaction. Microsoft, Amazon, Meta, and Alphabet collectively increased their AI infrastructure budgets from $670 billion to approximately $725 billion.

The overall earnings landscape remains solid, according to analysts. Corporate profit figures continue exceeding forecasts, while company guidance has proven more optimistic than anticipated given prevailing economic conditions.

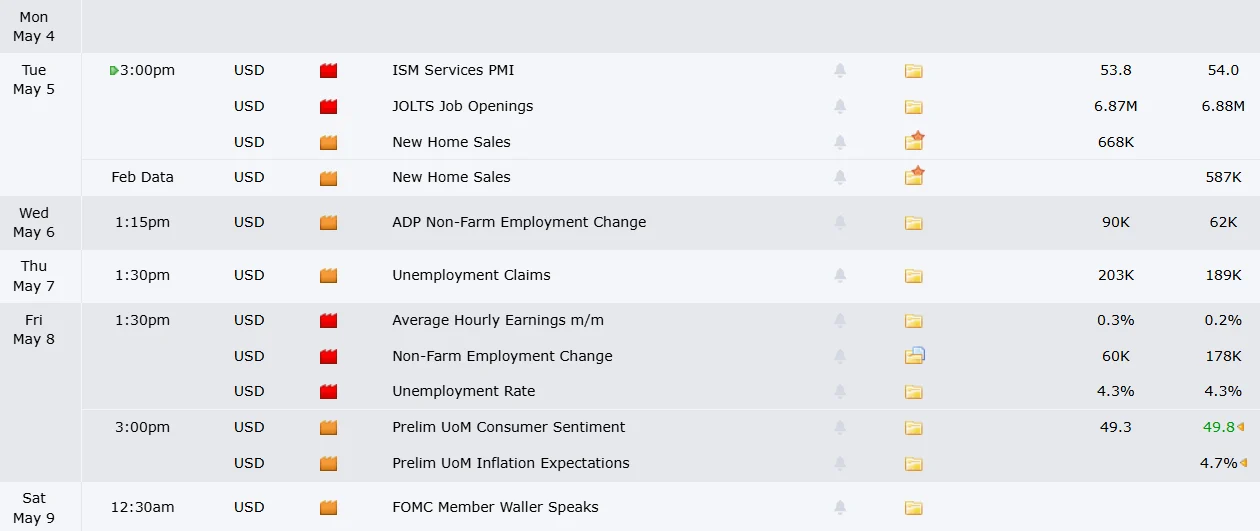

April Employment Report Commands Primary Attention

Friday’s release of April employment figures stands as the week’s most significant economic indicator. Projections call for roughly 60,000 positions added, representing a substantial decline from March’s 178,000 gain.

Weekly jobless claims reached their lowest point since 1969 last week, while ADP’s private sector employment data has displayed positive momentum. However, the previous 10 months have produced an inconsistent pattern of employment changes, complicating efforts to identify definitive trends.

The Federal Reserve maintains close surveillance of labor conditions. Policymakers continue evaluating their next interest rate decision while tracking employment alongside energy market fluctuations related to tensions with Iran.

Andrew Husby, economist at BNP Paribas, observes that AI-focused industries have experienced slower hiring patterns without significant workforce reductions. He characterizes this dynamic as “growing the labor pie with AI,” indicating technology’s role in expanding economic capacity beyond simple workforce substitution.

Additional labor market indicators arrive throughout the week: JOLTS job openings data on Tuesday, ADP private employment numbers on Wednesday, and Challenger job cut statistics on Thursday.

Chip Sector Results Provide AI Investment Reality Check

April delivered the semiconductor industry’s strongest monthly performance since February 2000, with the PHLX Semiconductor Index soaring over 40%. Advanced Micro Devices has rallied 70% during the past month heading into Tuesday’s earnings announcement. Arm Holdings has climbed 40%, while Lattice Semiconductor has gained 25%.

Lattice Semiconductor opens the reporting schedule Monday, followed by Advanced Micro Devices on Tuesday and Arm Holdings on Wednesday. These releases will clarify chip demand patterns as AI infrastructure investment intensifies.

AMD recently unveiled pricing increases and secured a substantial partnership with Meta. Analysts will scrutinize whether company guidance aligns with the optimistic spending signals from major technology players.

Steve Sosnick, strategist at Interactive Brokers, acknowledged the sector’s rapid gains create potential reversal risk, while noting that sustained positive earnings would challenge any bearish positioning.

Consumer Company Results Reveal Spending Patterns

Beyond technology and semiconductor sectors, consumer-oriented companies provide insights into household expenditure trends.

Walt Disney announces results Wednesday, with streaming subscriber growth and theme park attendance drawing particular focus. Marriott reports Wednesday and Airbnb on Thursday, as hospitality companies navigate elevated airfare costs and fuel expenses. United Airlines has indicated solid travel demand while anticipating pricing challenges during the year’s second half.

Quick-service restaurants also face scrutiny. Restaurant Brands, operator of Burger King and Popeyes, releases results Wednesday. McDonald’s follows Thursday with Wendy’s closing the week Friday. Budget-conscious consumers have reduced fast food purchases in recent months, prompting investors to seek evidence of demand stabilization.

Palantir launches the earnings cycle Monday after market close, with Novo Nordisk and Uber following on Wednesday.